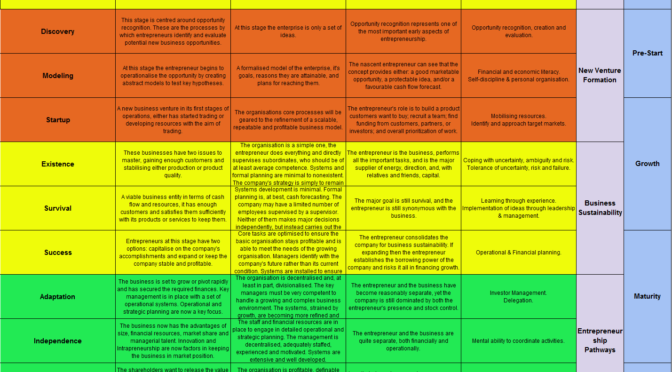

Introduction to Stage 5 – Survival

At this stage the business should be a viable entity in terms of cash flow and resources, it has enough customers and satisfies them sufficiently with its products or services to gain repeat sales. The organisation is still simple. The entrepreneur at this stage needs to be learning through experience on a daily basis. The company may have a limited number of employees supervised by a junior manager or supervisor. Neither of them makes major decisions independently, but instead carries out the defined orders of the entrepreneur. Formal planning is, at best, cash forecasting. The major goal is still survival, and the entrepreneur is still synonymous with the business. The entrepreneur starts to implement ideas through leadership and management which provide opportunities to scale.

Survival Stage Compendium

In the survival stage of a business lifecycle, the primary focus shifts towards sustaining operations and achieving a consistent cash flow, which will ensure the enterprise stays afloat. This stage is critical as it defines a thin line between the success and failure of a business. Various academic frameworks and real-world examples across the globe elucidate the survival stage’s significance and strategies to navigate it effectively.

- Academic Frameworks:

- According to Churchill and Lewis (1983), the survival stage necessitates generating sufficient revenue to cover expenses and beginning to attain a return on investments. The business model should be viable, with a clear market demand for the products or services offered (Churchill & Lewis, 1983).

- Small businesses often face challenges in managing resources, competition, and market dynamics. Academic discourse suggests implementing robust financial management practices, developing a loyal customer base, and adapting to market changes as pivotal survival strategies (Kuratko, D. F., Hornsby, J. S., & Covin, J. G., 2014).

- Global Examples:

- United States: Small businesses contribute significantly to the economy, yet they face a high failure rate, especially within the first five years. For instance, strategies like cost control, customer retention, and market differentiation have been key to survival for many small enterprises.

- Australia: The survival of small enterprises is a concern, given the competitive market environment. Businesses adopting innovative practices and government-supported initiatives have shown a higher survival rate (Department of Industry, Innovation and Science, Australia, 2018).

- United Kingdom: According to a report by the Office for National Statistics, small businesses that adopted digital technologies and engaged in e-commerce demonstrated a higher survival rate compared to those that did not.

The survival stage underscores the importance of financial stability, market adaptation, and innovation in ensuring business continuity. The insights from academic frameworks and real-world examples provide a holistic understanding of the survival stage, thereby assisting entrepreneurs in navigating the challenges and opportunities inherent in this critical phase of business development.

References:

- Churchill, N. C., & Lewis, V. L. (1983). The five stages of small business growth. Harvard Business Review, 61(3), 30-50.

- Kuratko, D. F., Hornsby, J. S., & Covin, J. G. (2014). Corporate Innovation: The Antecedents, Dimensions, and Outcomes of Entrepreneurial Orientation. European Management Journal, 32(6), 852-864.

- Department of Industry, Innovation and Science, Australia. (2018). Small Business Sector Report.

Entrepreneur Tips

The Survival stage in the business lifecycle is crucial as it requires a firm to not only sustain operations but also to work towards achieving consistent cash flow. Here are five tips to help entrepreneurs navigate through this stage:

- Financial Management:

- Maintain a strict budget and monitor your expenses meticulously. Effective financial management is key to survival. Utilize financial planning tools and consult with financial advisors to ensure you’re on the right track.

- Customer Retention:

- It’s often more cost-effective to retain existing customers than to acquire new ones. Focus on building strong relationships with your current customers, understand their needs, and work to exceed their expectations.

- Operational Efficiency:

- Streamlining operations to improve efficiency can help to reduce costs and improve service delivery. Assess your business processes, identify bottlenecks, and implement solutions to optimize operational efficiency.

- Market Adaptability:

- The market is constantly evolving; hence it’s crucial to stay updated with market trends and be ready to pivot your business model if necessary. Being adaptable to market changes can help in sustaining your business during tough times.

- Innovation and Continuous Improvement:

- Encourage a culture of innovation within your organization. Look for ways to improve your products or services, and be open to feedback from customers and employees. Continuous improvement can lead to better market positioning and customer satisfaction.

Following these tips, along with a disciplined and resilient approach, can significantly aid entrepreneurs in navigating the challenges inherent in the Survival stage of the business lifecycle.

Further Reading

View the original paper here, and the blogs in this series:

9 Stages of Enterprise Creation: Stage 1 – Discovery

9 Stages of Enterprise Creation: Stage 2 – Modeling

9 Stages of Enterprise Creation: Stage 3 – Startup

9 Stages of Enterprise Creation: Stage 4 – Existence

9 Stages of Enterprise Creation: Stage 5 – Survival

9 Stages of Enterprise Creation: Stage 6 – Discovery

9 Stages of Enterprise Creation: Stage 7 – Adaptation

9 Stages of Enterprise Creation: Stage 8 – Independence

9 Stages of Enterprise Creation: Stage 9 – Exit